Hispanic Millennials and Financial Services

This post outlines some of the findings from the 3rd Wave of the Hispanic Millennial Project, the groundbreaking study we’ve done in conjunction with Sensis.

- In Wave 1, we explored the Hispanic Millennials as a group and looked into the demographics and psychographics that define them, as well as their growth in the US and the buying power that comes with that.

- Wave 2 focused on Hispanic Millennials' attitudes and behaviors associated with healthcare… their health, diet, exercise, insurance, and many other key subjects.

In Wave 3, we look at Hispanic Millennials (HM) feelings and actions related to their finances. In addition to the research looking into the Hispanic community, in the phase, we also looked at White/non-Hispanic Millennials (NHM), Asian Millennials (AM) and African-American Millennials (AAM)… and compare and contrast all four groups.

You might think that American Millennials – of all ethnicities – would be in the same ballpark when it comes to their finances… and you'd be partially right. In some aspects of it, they are in lock-step. For example, when asked if they did not believe in using a traditional bank, approximately 30% in each group completely or somewhat agreed.

But what’s interesting is where they diverge from one another. For example…

Conservatives?

When asked if they paid off their credit cards “in full” each month, 49% of Hispanic Millennials completely or somewhat agreed, while Asian Millennials were at 61%. NHMs and AAMs were both at 46%.

Likewise, when asked if they had enough money put away for a “rainy day”, Asian Millennials came out on top at 54% vs. Hispanic Millennials at 48% (followed by non-Hispanics and African-Americans).

Are Asian Millennials more conservative with their money than the other groups? We’re not sure, but if you’re in the banking industry… you need to be paying attention.

Products

For most basic financial products – credit cards, checking & savings accounts, etc. – the familiarity with those products by each of the four groups runs about the same and at a very high rate. But a few products resonate at different levels.

For example, when asked how familiar they were with retirement savings plans (e.g. a 401k), 71% of African-American Millennials were very or somewhat familiar, but it dropped to 58% for Hispanics. Similarly, for ‘payday loans,” it was African-Americans at 65%... Hispanics at 49%. Finally, for the investment vehicle of Mutual Funds, it was African-Americans at 52%... Hispanics at 40%.

Why the big drop-off with Hispanic Millennials? They didn’t say… but for those businesses that sell those kinds of products, there exists a gap in the Hispanic community that needs to be filled.

Hispanics and Banking

Across the four Millennial groups, Hispanics have the most positive feelings toward banks and financial institutions, with 61% rating their opinion as very or somewhat positive, dropping to 55% for Non-Hispanic Millennials.

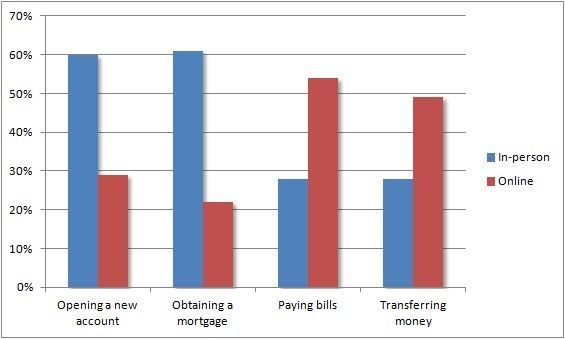

Interestingly, how they engage their banks vary, based on the activity needed. When opening a new account, 60% still want to do it in person, compared to just 29% who would rather go online. The same goes for obtaining a mortgage – 61% in-person vs. 22% online.

That dynamic completely shifts, however, when looking at other kinds of transactions… when paying bills, 54% of Hispanic Millennials would rather do so online vs. 28% in-person. Likewise when transferring money between accounts – 49% online and 28% in-person.

And while convenience, good customer service and low fees are important when selecting their banks, 34% of Hispanic Millennials say that “language factors” are very or somewhat important when choosing a financial institution, as much as 17% higher than the other groups.

Finally, while all four Millennial groups think all traditional banks are about the same (sounds like bank marketers needs to step up!), Hispanics are clearly the most adventurous when considering non-traditional institutions, while non-Hispanics are the least willing to try something new…

- 58% of HMs are open to non-traditional banks with no branches like Ally or Capital One, dropping to as low as 47% for non-Hispanics.

- For non-traditional banking companies like Amazon, Apple, Google or Facebook offering banking services, it’s 55% vs. 47%.

- And for non-traditional banking retailers like Wal-Mart or Target offering banking services, Hispanics were at 54%, 9 points higher than non-Hispanics.

Overwhelmed?

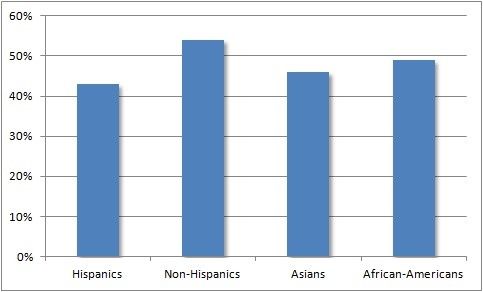

Perhaps the most intriguing of the questions – because it explored emotions – was about feeling “financially overwhelmed.” Here, Hispanic Millennials seemed to be on the most solid ground.

Only 43% of Hispanic Millennials completely or somewhat agreed that they were overwhelmed… lower than all the other groups:

Why is that? Are Hispanic Millennials more optimistic? Do they feel better because of the very strong family & community culture they live in?

So what does all of this mean? I think there are a few conclusions we can draw…

- Across the board, all four Millennials groups worry about their money… now and in preparation for the future.

- That each of the four groups – Hispanic Millennials, White/non-Hispanic Millennials, Asian Millennials and African-American Millennials – while similar in many regards on how they think about their finances, they are also very different and as such, need to be communicated-to in ways that are culturally-sensitive and appropriate.

- That there is an enormous opportunity for businesses in the financial sector – traditional banks, non-traditional banks, credit card company, investment firms and so on. And as the Millennials grow in numbers and buying power, businesses that don’t embrace them will lose out to their competitors.

To download the report which also explores several more areas related to Hispanic Millennials and their finances, Click Here. Stay tuned for our report focusing on Asian and African American Millennials.

We are pleased to offer free of charge the full contents of the report referenced in this blog entry. Please click the link below to get your copy now.